- Both stocks and bonds are selling off right now, a shift from their past relationship.

- Until the past few weeks, stocks continued to climb to records as bond prices fell.

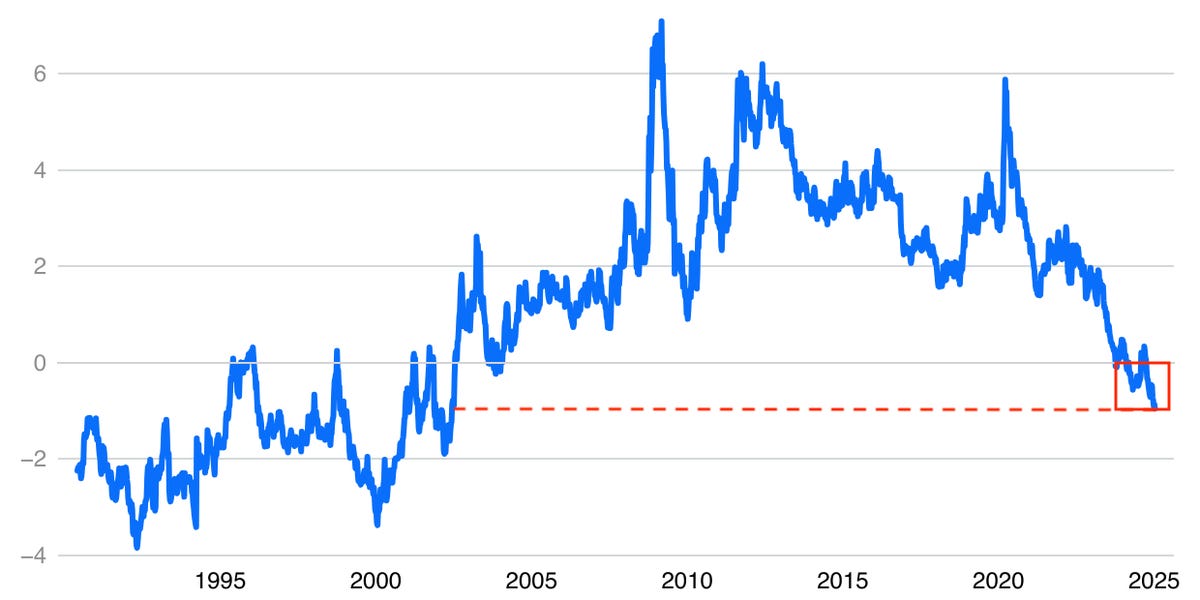

- Recently the S&P 500 earnings yield fell below the 10-year Treasury yield to a degree not seen since 2002.

It’s getting increasingly difficult to find returns in the market as stock and bond prices fall simultaneously.

The tandem sell-off is a relatively new dynamic. Until the past few weeks, stocks continued hitting new highs as bonds declined.

One development that helps explain this correlational shift is the relationship between the relative yields offered by the two assets. The gap between the S&P 500’s earnings yield and the 10-year Treasury yield has slipped into negative territory and is at its widest point since 2002. Put differently, the relative attractiveness of ultrasafe bonds versus everyday stocks is at its most pronounced in decades.

The resulting sell-off in stocks ultimately boils down to a valuation issue. If safer bonds are yielding more than them, are equities worth the cost and the risk as they sit near record highs?

Investors have decided the answer is no, at least lately. This view has become more prevalent as the luster around President-elect Donald Trump’s protectionist trade policies has worn off and traders instead focus on the impact higher borrowing costs could have on corporate earnings.

The question then becomes: Why aren’t bond prices rising? If stocks are losing steam, why aren’t investors piling into bonds as a clear alternative?

For one, traders are coming around to the idea that the Federal Reserve is going to drastically slow its pace of rate cuts, which has pushed yields higher. (Yields trade inverse to the price of bonds.) Some on Wall Street even think the Fed funds rate will go unchanged through 2025. This outlook was heightened on Friday after a blowout jobs report.

Further, investors are concerned that Trump’s proposed policies will stoke a rebound in inflation. Such a situation could then, in turn, necessitate further rate increases.

Stock market concentration risk

The situation in stocks is being compounded by the fact that much of the market’s success hinges on the performance of a handful of megacap tech companies, which have already delivered massive gains since the start of the bull market two years ago.

This was highlighted by a recent note from Goldman Sachs, which said the expected earnings growth of megacap tech companies was starting to narrow considerably relative to the other 493 companies in the S&P 500.

The so-called Magnificent Seven stocks are expected to grow earnings 18% in 2025 and 16% in 2026, compared with 11% and 13% for the other S&P 493 companies, the bank said.

“The S&P 500 looks expensive on a P/E basis and the earnings outlook remains highly unbalanced,” strategists at TS Lombard said. “The market is banking on sustained strong growth for the ‘Magnificent 7’ stocks.”

With so many uncertainties compounded by an incoming Trump administration that seems laser-focused on implementing policies that could spark a rebound in inflation, investors are left wondering why even take on so much risk in stocks when bond yields offer such appealing returns.